Meaning and definitions of Controlling

Controlling is the practice of ensuring that actual actions match up with planned ones and taking corrective measures to close gaps. It is a fundamental managerial task. It entails creating performance benchmarks or indicators, assessing actual performance, and acting appropriately when there is a discrepancy between the two. Hence, it also goes by the name of performance evaluation. This article will tell us about control, its definitions, features, types, significance, and many more aspects.

Checking, testing, regulating, verifying, or adjusting are all parts of the controlling process, which ensures an organization's mission and objectives are as effectively and efficiently achieved as possible. It is an ongoing managerial responsibility. It directs management in taking steps to boost future organizational performance. Controlling is carried out at all levels and locations. In other words, controlling is a management task that evaluates how closely actual results match predetermined objectives. It guarantees the effective and efficient use of resources to accomplish organizational goals. Controlling is a purpose-driven function, then. Some notable examples of definitions of control are discussed below.

According to Joseph L. Messie, "Control is the process of assessing current performance and directing it toward specific objectives."

According to Theo Haiman, "Control is the process of determining whether or not proper progress toward goals and objectives is being built and, if needed, acting to correct deviation."

According to George R. Terry, "Controlling entails assessing the performance and, if necessary, taking corrective action to ensure that it proceeds as planned."

According to Stephen P. Robbins, "Control is the process of observing operations to make sure they are carried out as intended and addressing any material deviations."

In conclusion, controlling is a managerial task that evaluates and contrasts actual and anticipated performance. If deviations are found, corrective measures should be taken to eliminate them. It ensures the right people do the right things at the right time. Controlling then serves as a managerial tool to improve organizational effectiveness. In summary, controlling is an administrative activity that assesses and compares actual performance to expectations.

Features or Characteristics of Control

In this section, we will learn about the features of control. Control is a management function that ensures the accomplishment of organizational goals and plans by monitoring performance and making adjustments as needed. For all kinds of organizations, a reliable control system is essential. It guarantees that the organization's goal is achieved under established standards. The characteristics or features of control are described below:

- A vital management function: Control is one of the fundamental managerial tasks. It is a procedure that guarantees that actual performance is consistent with plans and focused on achieving goals. As a result, every manager must oversee subordinate implementation to ensure that objectives are met.

- Pervasive function: Every level of management and every operation within an organization are covered by the holistic function of leadership known as controlling. The type and level of control vary depending on the management level and function. The Chief Executive Officer, for instance, has control over the Deputy General Managers. Deputy General Managers supervise Department Heads, who oversee Section Chiefs, and so forth. Depending on the type of organization, the control mechanism varies. The levels of control in the hierarchy descend as one moves up.

- Continuous process: Control is a never-ending or constant process. It will continue as long as the organization is in existence. Therefore, managers must ensure that employees consistently follow instructions and perform to expectations. This managerial task entails ongoing analysis and research of the organization's implementation strategies, policies, and procedures. Similar comparisons should be made between expected and actual performance, and corrective measures should be taken as necessary.

- Dynamic function: Control is flexible and active rather than rigid. Corrective actions produced by control may necessitate changes in other management functions. Therefore, the control system must be modified to accommodate the organization's shifting needs and conditions. In addition, the manager must modify current practices and implement new strategies to prevail. Therefore, the controlling system must adapt to change with the time, situation, environment, and organizational needs.

- Forward-looking: Control is always thinking forwards because it is always linked to the future. The past is inescapable. Only future actions can be improved by taking corrective action based on prior experience. The control function is intended to compare actual performance to expected performance, provide early warnings and information to detect errors and weaknesses, and take timely action to eliminate and minimize mistakes.

- Measurement and comparison: Control is a management activity that compares actual performance to expected performance. If there is a difference between actual and expected performance, the manager takes corrective action to close the gap. It aids in the achievement of the organization's predetermined goals within the constraints of time and resources.

- Related to planning: Planning and control have a close relationship. Planning entails setting goals and then deciding on the best course of action. While controlling seeks to ensure plan compliance, planning will only be successful if the implementation process is appropriately handled. According to academics, planning is the head, and controlling is the tail.

- Corrective action: If there is a critical deviation with negative causes, the manager should take disciplinary action to rectify the deviation. Corrective actions should be taken as soon as possible. It may include improving motivation, and training, making better use of available resources (workforce, money, materials, machines, etc.), changing predetermined standards, and so on. Corrective action must be taken tactfully and appropriately for the organization to improve.

A Quick Snapshot of Features of Control

Importance of Controlling

Controlling is an important management function that all managers must perform. A manager must exercise effective control over all activities of their subordinates to contribute to achieving organizational goals. Other management functions become meaningless in the absence of a proper controlling system. Therefore, the significance or importance of controlling can be deduced as follows:

- Execution of plan: Planning involves deciding what will be done ahead of time and bridging the gap between two points, i.e., where we are? where do we want to go? Control is the process of bringing performance into line with planned action. Controlling guides, the proper execution of plans. It determines whether or not actual work is performed following standards. Furthermore, it directs management to take the necessary actions if there are deviations between actual performance and predetermined criteria. Thus, the controlling function aids in returning the management cycle to planning. As a result, putting the plan into action is critical.

- Ensure better utilization of resources: Controlling assists in monitoring and supervising employee performance at all stages of operation. It also aids in the direction of all organizational activities to keep them on track. Hence, it ensures that all resources in an organization are used effectively and efficiently, with minimal waste and spoilage.

- Coordination tools: The expansion of business volume and activities necessitates the creation of new departments and sections to handle various functions. Controlling aids in providing a common direction to all activities of multiple departments and individual efforts to achieve organizational goals. As a result, it facilitates better goal-achievement coordination.

- Helps in supervision: The controlling process aids in comparing actual performance to predetermined standards, identifying deviations, and taking corrective action to ensure that activities are carried out as planned. Similarly, where there is a deviation in actual performance, management provides timely guidance and instruction to the relevant authority and employees. Controlling aids in the effectiveness of supervision and the maintenance of discipline among all administrative authorities.

- Psychological pressure: Employees are placed under extra pressure by the controlling function. When employees understand their functions and activities, which are monitored and supervised from the top level, they perform tasks more effectively and maintain discipline. As a result, it fosters an environment of order and discipline within the organization. It has been shown to boost employee morale and honesty.

- Delegation and decentralization of authority: Controlling ensures that delegated and decentralized authority of departments, sections, and subsections is used appropriately. Controlling defines activities and measures deviations so corrective actions can be implemented on time. As a result, management must develop a proper planning and control system to determine whether authority is being used properly.

In addition to the points mentioned above, increased efficiency, motivation, better management, risk minimization, basis for future action, productivity maximization, and cost minimization highlight the significance of controlling. Hence, control is an essential tool in the management arsenal.

Steps or Procedures of Controlling

1. Establishment of standards: The first step in the controlling process is establishing standards. The primary control areas of the organization are determined during this process, which is based on the organizational mission and goals. Performance standards are selected based on the mission and goals. A standard is a benchmark against which subsequent performance is measured. Managers can evaluate performance using criteria. Performance is typically measured in quantity, quality, time, cost, and behaviour, among other things. The standards that must be established fall into two categories:

- Tangible performance standards: Cost, expenditure, output, time, and so on are examples of tangible performance standards.

- Intangible standard: Intangible standards include employee morale, behaviour, management efficiency, ethics, and so on.

2. Measurement of performance: It is the second step in controlling. This step involves conducting regular assessments to ensure that plans, programs, projects, budgets, and procedures are on track to meet organizational goals. The goal is to take corrective actions in the event of deviations. Actual performance is measured here so that it can later be compared. Although measuring tangible standards is simple, measuring intangible standards is difficult. A robust management information system is required to measure an organization's performance.

3. Comparison of actual and standard performance: The actual performance should be compared to the standards after it has been measured. The comparison is performed to determine the difference (deviation) between actual and expected performance. If the performance meets the norm, the control process is terminated. Otherwise, efforts should be made to ascertain the causes of the deviations. This is the most crucial stage of the control process. During this process, organizations identify weaknesses and strengths in performance and take corrective action. Variations can be both positive and negative. Positive deviation indicates that actual performance exceeds expected performance differences. Positive deviation should thus be valued. The term "negative deviation" refers to the actual performance being lower than expected. As a result, management should pay close attention to the negative gap.

4. Analysis of causes of deviation: If the actual performances do not meet the established standards, there must be some reasons for deviations. Minor variations are typically disregarded. However, serious deviations need to be corrected right away. Therefore, conducting a thorough analysis of each performance aspect is crucial to identify and comprehend the reasons behind and consequences of deviations. Deviations may occur for various reasons, including internal flaws or environmental changes. A few weaknesses are a poor internal environment, a defect in the organizational structure's planning, a lack of raw materials, outdated technology, unsuitable production facilities, and a lack of coordination. The external factors include shifting technology, governmental regulations, rival businesses, etc.

5. Taking remedial action: The controlling process is close to this step. The management should take corrective action to close the gap after identifying the gap (especially the negative gap), its causes, and its effects. Reviewing plans, programs, goals, strategies, policies, motivational strategies, and training methodologies is also included in this step. To achieve standard performance, actions such as improving the machinery and equipment and using high-quality raw materials can be helpful.

Therefore, the actions mentioned above represent the majority of the controlling process. The steps must be studied to make controlling efficient, effective, and productive.

Pre-Control, Concurrent Control, and Post Control

Controlling is a function of management that compares actual performance to expected performance. If there are any deviations, corrective actions should be taken to resolve them. In other words, managerial activity ensures that organizational activities are directed in the right direction. There are various types of control, which are described below:

1. Pre-control:

This is the prudent or preliminary control. Pre-control attempts to identify and prevent violations of the standard before they occur. Pre-control pays close attention to the quality of human resources, materials, and financial resources to ensure the smooth flow of work. Pre-control emphasizes recruitment, selection, and placement to ensure that necessary, skilled individuals carry out the job. It places a premium on material procurement and ensures quality input for quality output. It is concerned with all aspects of the organization. By providing preventive measures, effective pre-control helps to reduce costs.

2. Concurrent control:

It is a continuous control. It oversees the organization's operations and ensures that standards are met throughout the process. For guiding employees' tasks and behaviour, concurrent control relies on performance standards, rules, and regulations. Simultaneous control aims to guarantee that work responsibilities produce the desired outcomes. If a deviation is discovered, it is corrected on the spot while the work is being performed. Concurrent control is also known as screening or Yes-No control. It frequently includes checkpoints where decisions are made about whether to continue progress, take corrective actions, or completely stop work on products or services. The transformation process is the focus of concurrent control.

3. Post-control:

Post-control entails reviewing the data to determine whether or not the performance meets the standard. This type of control focuses on the organization's output after the transformation is complete. It serves various vital functions and is known as feedback or output control. It is used when pre-control and concurrent control are either impossible or too expensive. Feedback or post-control provides managers with helpful information on how effective their planning effort was and serves as a guide to improve the planning process.

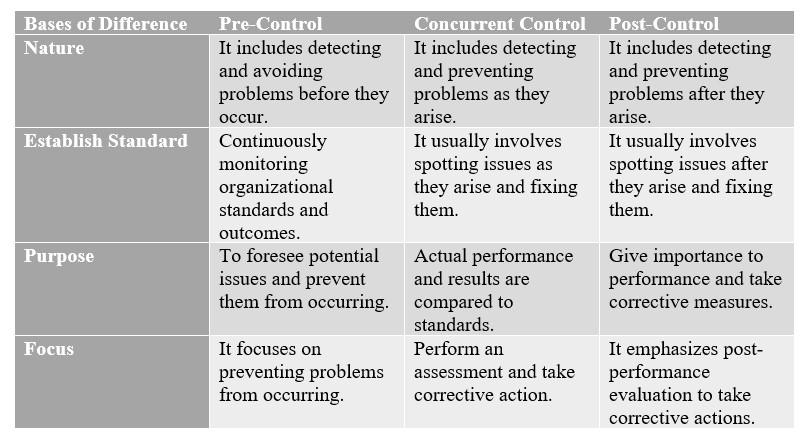

Difference between Pre-control, Concurrent Control, and Post Control

| Bases of Difference | Pre-Control | Concurrent Control | Post-Control |

|---|---|---|---|

| Nature | It includes detecting and avoiding problems before they occur. | It includes detecting and preventing problems as they arise. | It includes detecting and preventing problems after they arise. |

| Establish Standard | Continuously monitoring organizational standards and outcomes. | It usually involves spotting issues as they arise and fixing them. | It usually involves spotting issues after they arise and fixing them. |

| Purpose | To foresee potential issues and prevent them from occurring. | Actual performance and results are compared to standards. | Give importance to performance and take corrective measures. |

| Focus | It focuses on preventing problems from occurring. | Perform an assessment and take corrective action. | It emphasizes post-performance evaluation to take corrective actions. |

Essentials of Effective Control System

This final section of the article tells us about the essentials of an effective control system. Controlling is a crucial management function required in all types of organizations. The following are some of the essential components of an effective controlling system:

- Suitability: Every organization, large or small, is unique. Similarly, environmental changes in the organization happen quickly. As a result, the control system must be adaptable to changing conditions. It is thus critical to have a suitable controlling method that can be changed as needed and is flexible enough to be adjusted as needed. Furthermore, it must be appropriate for the organization's nature and requirements.

- Simplicity: Control systems should be clear, simple, and easy to understand by supervisors and subordinates. The management has to introduce a control system understood by every level employed. The complex and rigid system must be avoided to cope with changes. So, the control system should be straightforward.

- Economy: Another requisite for a good control system is cost-effectiveness. The controlling system should be within the organization's financial capabilities. The benefit of a control system should outweigh the cost of putting it in place. As a result, an excellent controlling system adds value to the organization while posing no financial burden.

- Objectivity: All of the organizations were founded with specific goals in mind. As a result, the controlling system must meet the organization's objectives. Controlling systems must have explicit goals. The primary purpose of the controlling system is to achieve standard performance. Modern tools and techniques are critical to meet the expected performance requirements.

- Flexibility: A control system must adapt to the business environment's changing complexities. This is a necessary component for maintaining the validity of a control system. A rigid control system would be ineffective in a changing environment. The control mechanism should conform to the new task standard as the task standard changes.

- Motivating: Motivation refers to empowering and energizing an individual to perform at their best without using external forces. As a result, the control system must be positive and creative to motivate subordinates. A sound control system also takes human factors into account. The primary goal of the human element is to save employees from errors rather than to punish them.

- Capable of communicating: The process of transmitting information from one person to another in an understandable language is known as communication. A sound control system should be simple, advanced, and efficient. This is because a control system must effectively communicate critical information to the relevant unit and authorities. The control process should communicate any deviations that require corrective actions at the appropriate time.

- Forward-looking: A sound control system should always be forward-thinking. Although past events and incidents cannot be controlled, the knowledge and experience gained from them can be used to avoid similar deviations in the future. All potential deviations should be corrected as soon as possible so that similar variations do not occur in the future.

- Acceptance: Acceptability is another critical component of a good control system. Employees should accept it at all levels. It is only meaningful if subordinates and different levels of management take it. The organization needs a more balanced control system to achieve its goals and motivate its employees. It is regarded as a burden.

Conclusion

To wrap up, controlling ensures that actual actions correspond to planned ones and takes corrective actions to close gaps. It entails developing performance benchmarks or indicators, assessing actual performance, and acting appropriately when the two differ. Controlling is then used by managers to improve organizational effectiveness. Controlling is an administrative activity that evaluates and compares actual performance to expected performance.

.jpeg)

{kind=link}

0 Comments

If this article has helped you, please leave a comment.